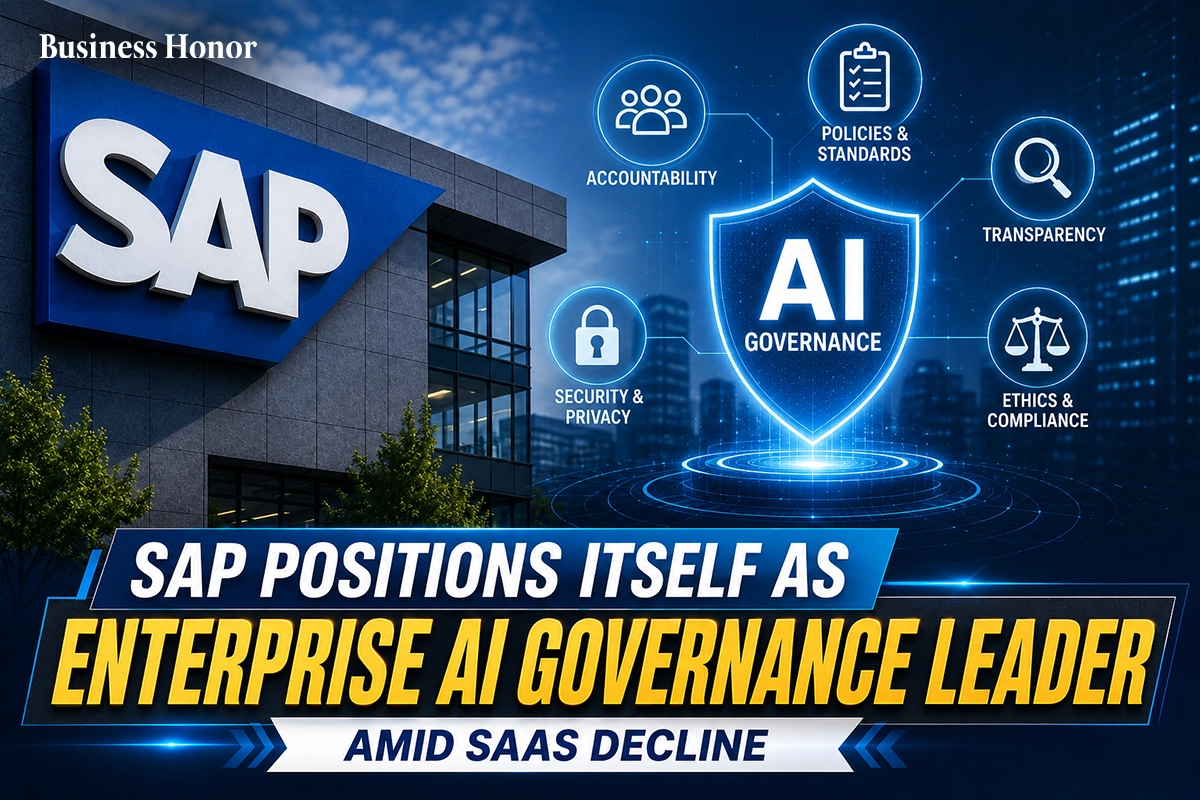

AI governance shifts from post-deployment audits to real-time enforcement, preventing financial system breaches before they occur in live environments.

|

One major issue with how businesses have typically overseen the use of AI systems in software is that most audits evaluate logs and AI governance after the AI has already produced its recommendation or output. This is fine for a system where AI is simply an auxiliary function (e.g., a chatbot that does not directly change the operation of the core enterprise), but for systems that involve managing strictly regulated financial information, this approach is entirely inadequate. For example, an ERP (enterprise resource planning) system includes controls over general ledgers, bank reconciliation, and journaling. By the time an audit examines logs of actions performed by an AI agent writing software code that violates established accounting principles, the integrity of the books and records has already been compromised—the books will be out of balance, there will be gaps in the auditing trail, and there will be significant damage to the business's overall accounting records.

Researchers developing systems such as ERPClaw—a specifically designed ERP that will allow generative AI to function safely within the context of financial transaction processing—have moved away from the "wait and review" audit paradigm and have instead created data integrity rules that are embedded and enforced within the architecture that supports AI functionality. According to researchers, the underlying assumptions of a business are termed the "constitution."

Each of these rules is checked at the time a proposed change is being made by using an Abstract Syntax Tree (AST) analyzer to verify the accuracy of the proposed code before it is executed in the live system. If an AI were to try to create a soft-delete capability for a journal entry, it would immediately violate the first rule of the constitution; therefore, no such capability would ever be permissible at the point of checking into the system. All enforcement of the rules will occur automatically with a binary confirmation of enforcement—there will be no exceptions.

The truly innovative feature of the enforcement of these accounting rules will be the creator of the enforcement—the design of the enforcement of these accounting rules will not only rely on deterministic automated code checking, but will also utilize a second agent which will only have a single function; to detect when an accounting rule has been violated. The code-forming agent and audit agent will work parallel to each other, and the difference between them is that the audit agent will check whether the proposed code can execute as permitted under US Constitution of whatever is being programmed into an enterprise system.

While it may seem that the audit agent needs to have greater capabilities than the generation agent does, this is not the case. In fact, the audit agent must be specific to the task of creating integrity rules and have no knowledge about business rule or user requests, allowing it to perform the auditing function with greater accuracy than a generalist system would. The audit agent acts as an adversarial agent with a reward structure that favors identifying a violation rather than validating such a violation.

Business Honor is of the view that constitutional AI enforcement represents a fundamental reimagining of enterprise system integrity and operational governance.

.webp)