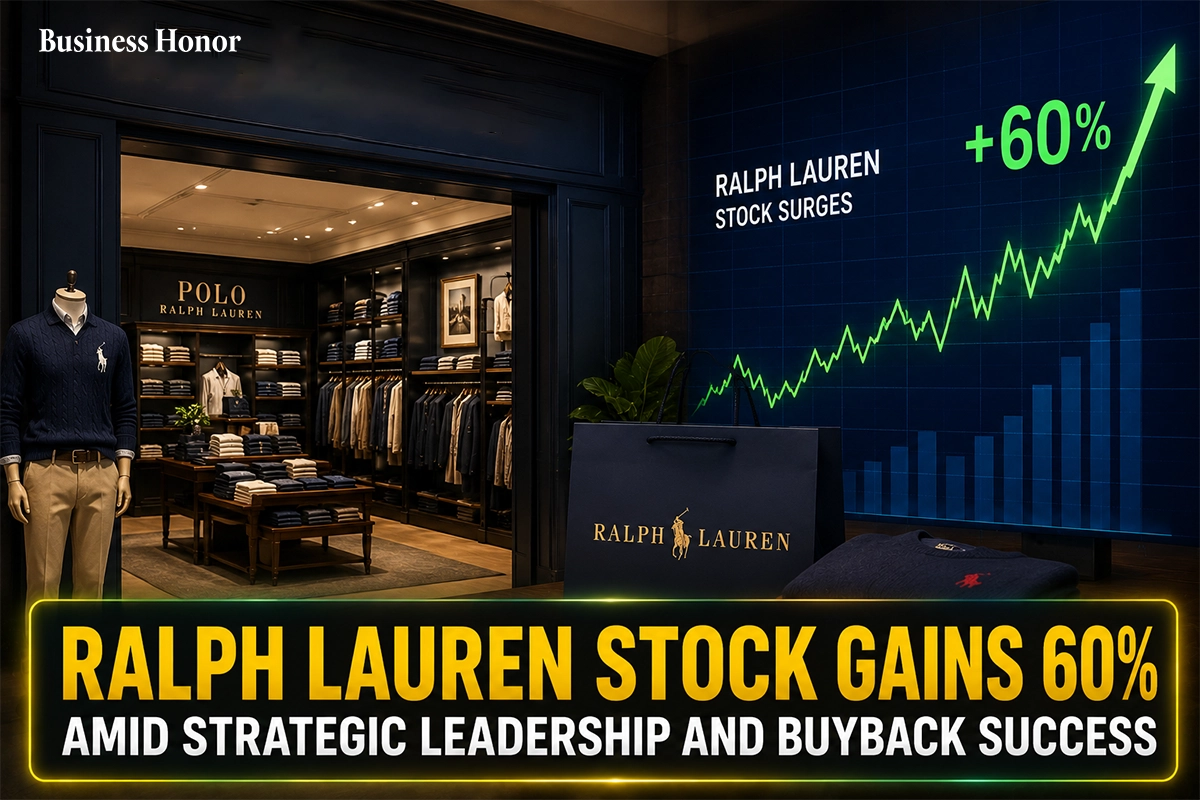

Ralph Lauren emerges as apparel standout with exceptional 2025 performance and disciplined capital allocation strategies implemented.

|

Jim Cramer, a highly regarded finance expert and analyst, has reaffirmed his previous view that Ralph Lauren Corporation is a tremendous investment opportunity ("a phenomenal winner") in light of the struggles that many other companies in the apparel sector have experienced this year. In his latest report, Cramer praised Ralph Lauren for generating great returns but also for its approach to managing itself in a disciplined and sophisticated manner. He noted that in 2025, Ralph Lauren stock had moved up by about 60% versus the S&P 500 and had drastically outdone the index in terms of stock price performance. But that it only started to outperform after the end of 2015 when it executed approximately 34.1% of its shares through share buybacks; until then, it had performed similarly to the entire stock market.

Cramer also gave credit to Ralph Lauren's CEO Patrice Louvet for all the success the company has had, showing tremendous confidence in Louvet's abilities to lead the organization. Cramer said, "I think the world of him ... I'm a huge fan of Patrice Louvet." He said Louvet is moving Ralph Lauren towards a safer type of growth by making the company's share price appreciation driven by "consistent margin expansion" versus aggressive aspirations for stock appreciation will resonate well with the investing community.

During an Investor day event hosted by Ralph Lauren, the company presented its long-term targets for revenue, earnings and free cash flow growth over the next three years. While the company’s projections did not meet the level of excitement that Jim saw in some of the prior year’s announcements, for instance, the stock is being acquired by another firm. It did reassure Jim that there were several key operating principles which would support management’s long-term goals (i.e., 1) continuing to drive top line revenue growth through three key growth initiatives, 2) developing long-term profitability at a rate of about 15% per annum, and 3) achieving consistency in margins despite having difficulty in other areas). In addition, Jim believed that Ralph Lauren's strong ability to improve its operating margin is a result of having good management practices that are significantly different from those of its competitors, many of which are having trouble generating profits.

From a valuation standpoint, Jim believes that Ralph Lauren is reasonably priced in light of the company’s expected growth in earnings. Currently, the stock is trading for approximately 20 times earnings that is significantly below the S&P500’s average multiple of nearly 25. In addition, Jim sees a strong difference in the company’s expected earnings growth rate of nearly 20% for this year versus the expected growth rate of just 9% for the entire S&P500® index. Due to this situation, Jim believes that the discount in value for the stock is not warranted given Ralph Lauren's superior growth potential.

Business Honor is of the view that Patrice Louvet's CEO leadership represents a strategic transformation in Ralph Lauren's operational execution and margin expansion capabilities.

.webp)